Beginner’s List: The 4 Types of Investment Accounts Explained

Investing is not just about picking the right stock; it is about choosing the right home for your money. Imagine your wealth as water. Before you decide what kind of water you want (stocks, bonds, ETFs), you need to decide which bucket to pour it into. The bucket determines how much water you get to keep (taxes) and when you can drink it (withdrawal rules).

For beginners, the financial jargon can be paralyzing. 401(k), Roth IRA, HSA, Brokerage—it sounds like alphabet soup. But understanding these four “buckets” is the single most important step in building generational wealth. It is a core discipline shared by those who have mastered the 7 habits of people who are good with money. This guide will demystify the four essential investment accounts so you can stop saving and start building.

Why Most People Never Start Investing (And How to Fix That)

The statistics on American investing participation are stark: roughly half of US adults have no money invested in the stock market whatsoever. Among those who do invest, the majority do not utilize all four account types available to them, leaving significant tax advantages unclaimed and future wealth unrealized. Understanding why people do not start investing—and systematically addressing those barriers—is the real starting point for this guide.

The most common barrier is perceived complexity. Investment account terminology is genuinely confusing to newcomers, and the financial services industry has historically done a poor job of simplifying it. The second barrier is perceived minimum requirements—many people believe they need a large sum before they can begin, when in reality most brokerages now allow account opening with zero minimum balance and fractional share purchases for as little as $1. The third barrier is fear of loss—the visceral discomfort of watching an investment value decline, amplified by media coverage that sensationalizes market drops.

Each of these barriers dissolves with understanding. Complexity is addressed by this guide. Minimum requirements have been eliminated by modern brokerages. Fear of loss is neutralized by understanding time horizon: for investments held over 10, 20, or 30 years, short-term market fluctuations become statistical noise. The S&P 500 has never produced a negative return over any 20-year period in its history. The risk is not in investing—it is in not investing.

The ten-year difference in the example above—same amount, same return, same ending age—produces nearly double the outcome purely through earlier starting. This is the mathematical argument for beginning immediately rather than waiting until you feel “ready” or until you have “more to invest.”

1. The Philosophy: It’s All About Taxes

Before we name the accounts, you must understand why they exist. The government creates these accounts to incentivize you to save for your own future. In exchange for locking your money away until retirement, they offer you tax breaks.

Generally, tax advantages come in two flavors:

- Tax-Deferred (Traditional): You don’t pay taxes on the money now. It lowers your tax bill today, but you pay taxes when you withdraw it in retirement.

- Tax-Exempt (Roth): You pay taxes on the money now, but it grows tax-free forever. You pay zero taxes when you withdraw it in retirement.

Understanding this distinction is as crucial as understanding the steps to improve your credit score fast. It determines your long-term net worth.

Understanding Tax Brackets and Why They Change the Calculus

The traditional vs. Roth decision is fundamentally a tax rate arbitrage question: do you pay taxes at your current rate (Roth) or at your retirement rate (Traditional)? Getting this decision right requires understanding how tax brackets work and making an informed prediction about your future tax situation.

The US federal income tax system is marginal—each dollar of income is taxed at the rate of the bracket it falls into, not at a single flat rate applied to all income. A person in the “22% bracket” does not pay 22% on all their income; they pay the lower bracket rates on the first portions of income and only pay 22% on the income that falls within that bracket. Understanding this prevents the common mistake of refusing a raise because “it’ll push me into a higher bracket”—only the additional income above the threshold is taxed at the higher rate.

For the traditional vs. Roth decision: if you are early in your career, your current income is likely lower than your peak earning years will be, and your future retirement income may be lower than your current income. In this situation—low current tax rate, uncertain future rate—the Roth IRA is frequently the better choice. You pay taxes now at a low rate and receive tax-free growth and withdrawals forever. If you are in your peak earning years and expect a significant income decline in retirement, Traditional accounts defer taxes from a high-rate period to a lower-rate period, producing genuine tax savings.

The safest strategy for most people who are uncertain about future tax rates is diversification across tax treatment: maintaining both Traditional and Roth accounts simultaneously. This creates optionality in retirement—the ability to draw from whichever account type produces the lower tax bill in a given year, based on the actual tax environment at that time.

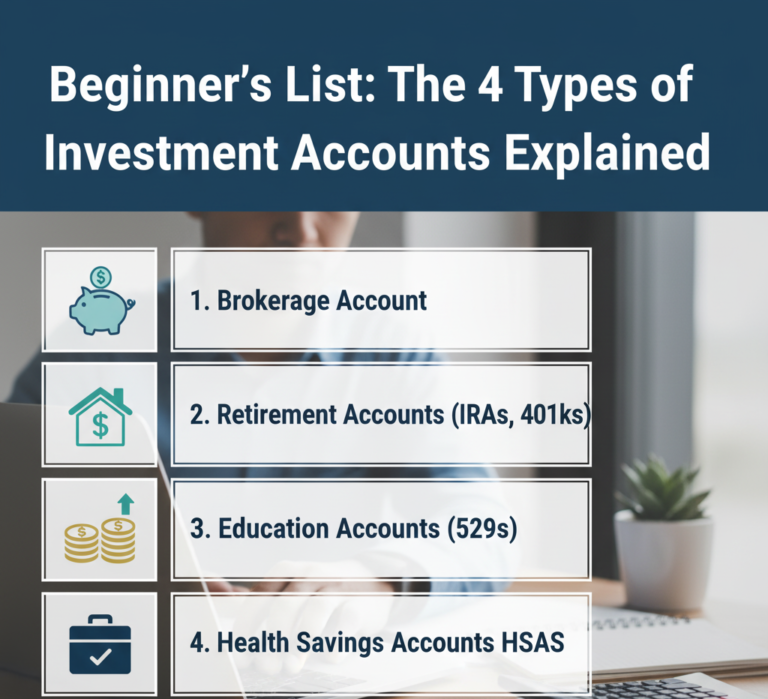

Account Type 1: The Employer Plan (401k / 403b)

This is the “Free Money” bucket. It is offered by your employer and usually deducted directly from your paycheck before you even see the money.

The “Match” is Magic

Most employers offer a “match.” For example, if you contribute 3% of your salary, they contribute 3%. That is an instant, guaranteed 100% return on your investment. No stock in the world offers a guaranteed 100% return.

Key Features:

- Contribution Limit (High): You can contribute a significant amount annually (over $20k), far more than other accounts.

- Automation: Because it comes out of your paycheck, it forces you to save. This automation is a key productivity hack, similar to using the best productivity apps to manage your tasks.

- Limited Choices: You are usually limited to a small menu of mutual funds selected by your employer.

Maximizing Your 401(k): Beyond the Match

The employer match is the headline feature of a 401(k), but experienced investors know that optimizing the account extends significantly beyond capturing the match. The investment menu—typically 10–30 fund options selected by your employer—varies enormously in quality. Some employers offer excellent low-cost index funds; others offer only high-fee actively managed funds that erode returns over time.

The metric to evaluate every fund option in your plan is the expense ratio—the annual percentage of your investment that the fund charges for management. A 0.05% expense ratio (common in index funds from Vanguard, Fidelity, or Schwab) vs. a 1.0% expense ratio (common in actively managed funds) represents a 0.95% annual drag on returns. On a $100,000 balance over 30 years at 7% annual growth, that difference compounds to approximately $85,000 in lost returns from fees alone. Always select the lowest expense ratio option available for each asset class you want to own.

The Roth 401(k) option—now available in many employer plans—allows after-tax contributions that grow and withdraw tax-free, combining the Roth IRA’s tax structure with the 401(k)’s higher contribution limits. For younger employees or those who expect their future tax rate to exceed their current rate, maximizing the Roth 401(k) rather than the Traditional 401(k) can produce substantially better after-tax retirement outcomes.

Vesting Schedules: The Hidden Risk of Employer Matches

The employer match is not always immediately yours. Most companies apply a vesting schedule—a timeline over which you gradually earn ownership of the employer’s contributions. A three-year cliff vesting schedule means you forfeit all employer contributions if you leave before year three; a graded schedule might give you 20% per year for five years.

Understanding your vesting schedule is essential before making career decisions. Leaving a job one month before your match vests can cost you thousands of dollars. Conversely, staying at a job primarily to complete a vesting period is a financial consideration worth weighing against the opportunity cost of career advancement elsewhere.

Account Type 2: The IRA (Traditional & Roth)

This is the “Freedom” bucket. Unlike the 401(k), this account is not tied to your job. You open it yourself at a brokerage (like Vanguard, Fidelity, or Schwab), giving you total control.

Traditional IRA vs. Roth IRA

This is the most common question in personal finance.

- Traditional IRA: You get a tax break today. Good if you are a high earner now and expect to be in a lower tax bracket when you retire.

- Roth IRA: You pay taxes today, but the growth is tax-free. This is generally preferred for younger investors or those in lower tax brackets, as decades of compound interest will be tax-free.

Funding an IRA often requires finding “extra” money in your budget. Use our zero-based budget checklist to identify waste in your spending that can be redirected here.

The Roth IRA’s Hidden Flexibility Advantage

The Roth IRA has a feature that most financial guides undersell: contribution withdrawal flexibility. Unlike Traditional IRAs and 401(k)s where any early withdrawal triggers taxes and a 10% penalty, Roth IRA contributions (not earnings) can be withdrawn at any time, for any reason, with no taxes or penalties. You already paid tax on that money—the IRS has no additional claim on it.

This feature makes the Roth IRA simultaneously the best retirement account for most young investors and a surprisingly flexible financial tool. Contributions made today can serve as an emergency fund of last resort—money that grows tax-free in invested assets but can be accessed penalty-free if a genuine financial crisis requires it. This dual function makes the Roth IRA particularly valuable for people who are nervous about “locking up” money in a retirement account.

The critical distinction: only contributions can be withdrawn penalty-free early. Earnings on those contributions are subject to the standard early withdrawal rules (taxes plus 10% penalty) until age 59½. The five-year rule also applies—the account must have been open for at least five years before earnings can be withdrawn tax-free.

Income Limits and the Backdoor Roth Strategy

Roth IRA contributions are subject to income limits that phase out at higher incomes. For high earners who exceed these thresholds, direct Roth IRA contributions are partially or completely prohibited. The backdoor Roth IRA is the widely-used legal strategy to circumvent this limitation: make a non-deductible Traditional IRA contribution (which has no income limit) and immediately convert it to a Roth IRA. The conversion is a taxable event only on the earnings between contribution and conversion—if converted immediately, the tax is essentially zero.

This strategy requires careful execution if you have other pre-tax Traditional IRA balances, due to the IRS’s pro-rata rule which determines the taxable portion of any conversion. A tax professional or fee-only financial advisor can confirm whether the backdoor Roth makes sense given your specific account situation.

Account Type 3: The HSA (The “Stealth” Investment Account)

Most people think the Health Savings Account (HSA) is just for buying bandages and glasses. They are wrong. For the savvy investor, the HSA is the ultimate retirement vehicle. It is the only account with a “Triple Tax Advantage.”

The Triple Threat

- Tax Deduction: Money goes in tax-free (lowers your taxable income).

- Tax-Free Growth: If you invest the funds, they grow without being taxed.

- Tax-Free Withdrawal: If used for qualified medical expenses, you pay zero tax on withdrawal.

The Strategy:

Don’t spend your HSA money on small medical bills now if you can afford to pay cash. Let the HSA grow like an investment account for 20 or 30 years. In retirement, you can use it for healthcare costs (which will be high). This is a long-term play that requires the discipline found in the top 5 habits of highly effective people.

HSA Deep Dive: How to Actually Invest Inside Your HSA

Many HSA account holders leave their balance sitting in a low-interest cash account, unaware that most HSA providers allow—and encourage—investing the balance in mutual funds or ETFs once a minimum cash balance threshold is met. This untapped investment capacity is where the HSA’s triple tax advantage becomes transformative.

The mechanics: open an HSA with a provider that offers robust investment options and low fees (Fidelity’s HSA is widely considered the best, offering zero monthly fees and access to thousands of no-fee index funds). Contribute the annual maximum. Maintain a small cash buffer—perhaps $1,000–$2,000—for potential near-term medical costs. Invest the remainder in a low-cost index fund. Do not touch it for years or decades.

The receipt strategy supercharges the HSA’s long-term value: keep digital or physical copies of every qualified medical expense you pay out-of-pocket. The IRS does not impose a time limit on HSA reimbursements—an expense from ten years ago can be reimbursed today if you have the receipt. This means you can accumulate decades of qualified medical expenses and withdraw the equivalent amount from your HSA tax-free at any time, effectively converting HSA dollars to tax-free cash while the investment balance has compounded untouched.

HSA Eligibility: The High-Deductible Health Plan Requirement

HSA eligibility requires enrollment in a qualifying High-Deductible Health Plan (HDHP). This means the HSA strategy is not available to everyone—it requires selecting an HDHP during open enrollment rather than a traditional PPO or HMO plan. For many healthy individuals and families whose actual medical utilization is low, the premium savings from an HDHP combined with the HSA’s tax advantages more than compensate for the higher deductible. Running the numbers for your specific health utilization history is essential before making this election.

People with chronic conditions, high medication costs, or expected significant medical utilization in the coming year should evaluate the HDHP vs. traditional plan trade-off carefully before assuming the HSA strategy is right for them. The triple tax advantage is valuable; paying thousands of dollars more in out-of-pocket medical costs to access it may not be.

Account Type 4: The Taxable Brokerage (The “Bridge” Account)

This is the “Liquid” bucket. The first three accounts penalize you if you touch the money before age 59½. The Taxable Brokerage account has no such rules. You can put money in today and take it out tomorrow.

Flexibility Comes at a Cost

Because there are no restrictions, there are no tax breaks. You invest with after-tax money, and you pay “Capital Gains Tax” on any profit you make when you sell.

Why You Need It:

- Early Retirement: If you plan to retire before 59½ (the FIRE movement), you need this “bridge” money to live on until your retirement accounts unlock.

- Big Goals: Use this for mid-term goals (5-10 years away), like buying a house or funding a dream trip to the cheapest European cities.

Managing a taxable account requires organization. Dedicate a block of time to review it monthly, using the principles from the complete guide to time-blocking.

Tax-Efficient Investing in a Taxable Account

Because taxable accounts lack the tax shelter of retirement accounts, the investments you hold in them and how you manage them determines a significant portion of your after-tax returns. Tax efficiency in a taxable account is a genuine skill that compounds over time.

Hold period matters enormously. Short-term capital gains (assets held less than one year) are taxed as ordinary income—potentially at rates of 22–37%. Long-term capital gains (assets held more than one year) are taxed at preferential rates of 0%, 15%, or 20% depending on your income. Simply holding investments for over a year before selling—the “buy and hold” approach—reduces your tax rate on gains by potentially half or more compared to frequent trading.

Tax-loss harvesting is the practice of selling investments at a loss to offset gains elsewhere in the portfolio, reducing your taxable capital gains for the year. The sold investment is immediately replaced with a similar (but not identical, due to the IRS “wash sale” rule) investment to maintain portfolio exposure. Automated investment platforms increasingly offer this feature as a standard service; manual practitioners typically review their portfolio in November for harvesting opportunities before the tax year closes.

Asset location strategy optimizes which investments are held in which accounts. Assets that generate regular taxable income (bonds, REITs, high-dividend stocks) are most efficiently held in tax-sheltered accounts where their income is not taxed annually. Tax-efficient assets (broad market index funds with low turnover and minimal dividends) are most appropriately held in taxable accounts where they generate little annual tax drag. Applying this logic across your full portfolio—treating all accounts together as a single optimized system—can meaningfully improve after-tax returns over decades.

3. The “Waterfall” Method: Where to Put Your Dollar First

Now that you know the accounts, in what order should you fill them? Financial experts generally recommend this “Waterfall” hierarchy to maximize efficiency:

- 401(k) Match: Contribute just enough to get the full employer match. (Free money).

- High-Interest Debt: Pause investing to kill credit card debt. (Guaranteed return).

- HSA (If eligible): Max this out for the triple tax benefit.

- Roth IRA: Max this out for tax-free growth and flexibility.

- 401(k) Remainder: Go back and fill the rest of your 401(k) space.

- Taxable Brokerage: Any leftover money goes here.

This strategy ensures you are prioritizing high-impact actions, a concept central to beating procrastination in your financial life.

What to Actually Invest In: The Beginner’s Asset Selection Guide

Knowing which accounts to use is the first level of investing literacy. Knowing what to put inside those accounts is the second level. For most beginners and even many experienced investors, the evidence overwhelmingly supports a simple, low-cost index fund approach over individual stock selection or actively managed funds.

Index Funds and ETFs: The Evidence-Based Choice

An index fund is a type of mutual fund or ETF that tracks a specific market index—the S&P 500, the total US stock market, the total international stock market—by holding all or most of the securities in that index. Rather than a fund manager actively selecting stocks, the fund passively replicates the index, which produces two powerful advantages: lower costs (no expensive research team required) and returns that match the market rather than attempting to beat it.

The underperformance of actively managed funds relative to their index fund benchmarks is one of the most consistently documented findings in financial research. Over any 15-year period, more than 85% of actively managed US large-cap funds underperform their index benchmark after fees. The minority that do outperform in one period does not consistently outperform in subsequent periods. For a long-term investor, the rational conclusion is to own the index and pay minimal fees.

The three-fund portfolio—a combination of a total US stock market fund, a total international stock market fund, and a total bond market fund—is the simplest evidence-based portfolio construction that provides broad diversification, low cost, and hands-off simplicity. Adjusting the allocation between these three funds based on your age and risk tolerance provides all the customization most investors genuinely need.

Target-Date Funds: The Autopilot Option

For investors who want to invest appropriately without ever making an asset allocation decision, target-date funds are the closest thing to a complete solution. These funds automatically adjust their allocation from aggressive (more stocks, fewer bonds) in early years to conservative (fewer stocks, more bonds) as the target retirement date approaches. You select the fund with the year closest to your expected retirement—a 2055 fund for someone planning to retire around that time—and the fund manages the rest.

Target-date funds are the recommended default for 401(k) investors who are not ready to select individual funds from the plan menu. Their expense ratios vary widely—Vanguard’s target-date funds charge approximately 0.08–0.15%, while some employer plan options charge 0.5–1.0%. Always check the expense ratio before selecting, even for target-date funds.

How to Open Each Account: A Step-by-Step Walkthrough

Understanding the accounts theoretically is valuable. Actually opening them is what changes your financial trajectory. This section walks through the practical process for opening each account type so there is no ambiguity between reading this guide and taking action.

Opening a 401(k)

The 401(k) enrollment process is initiated through your employer’s HR department or benefits portal. If you are a new employee, you are typically presented with enrollment options during onboarding; if you have been with your employer for a while and have not enrolled, contact HR directly—you can enroll during the annual open enrollment period or, in many plans, at any time.

The enrollment decisions you will make: your contribution percentage (start with at least the match percentage; increase by 1% per year until you reach a comfortable maximum), your investment selection from the available menu (select the lowest-cost index fund options or a target-date fund), and your beneficiary designation (critical—the beneficiary on your retirement account supersedes your will and determines who receives the account upon your death). Review and update your beneficiary after any major life event.

Opening an IRA or Roth IRA

IRA accounts are opened directly with a brokerage institution. The three most commonly recommended for beginners are Fidelity (known for excellent customer service and zero minimum balance), Vanguard (the pioneer of index fund investing with the lowest costs in the industry), and Schwab (strong combination of low costs and accessible interface). All three allow online account opening in approximately 15 minutes.

The information you will need: Social Security number, bank account information for funding, and basic personal and employment information. After opening, connect your bank account for transfers, make your initial contribution, and immediately select your investments—contributions left in the default cash position do not benefit from market growth.

Opening an HSA

HSA access is tied to your health insurance enrollment. If you are enrolled in a qualifying HDHP through your employer, your employer typically designates an HSA provider and may offer the option to contribute via payroll deduction (which provides an additional FICA tax savings not available through direct contribution). If your employer does not offer payroll deduction or you are self-employed with an HDHP, you can open an HSA directly with providers like Fidelity or Lively and make direct contributions.

Opening a Taxable Brokerage Account

Taxable brokerage accounts can be opened at the same institutions as IRAs—Fidelity, Vanguard, Schwab—and the process is nearly identical. The account type selected at opening determines the tax treatment; ensure you select “individual taxable” or “joint taxable” account rather than an IRA type. No contribution limits apply; you can deposit any amount at any time from any funding source.

The Most Costly Investment Mistakes Beginners Make

The investment journey is well-documented enough that the most common beginner mistakes are predictable and preventable. Knowing them in advance—rather than learning through expensive experience—is one of the most valuable forms of financial education.

Waiting for the “Right Time” to Invest

Market timing—the attempt to invest when prices are low and sell when prices are high—is one of the most thoroughly debunked strategies in finance. It fails for two reasons: markets are unpredictable in the short term (even professional fund managers with entire research teams fail to consistently time markets correctly), and the cost of being out of the market during its best days is catastrophic to long-term returns. A significant portion of the market’s total long-term return occurs in a very small number of high-return days; investors who are out of the market on those days miss returns that are never recovered.

The evidence-based alternative is dollar-cost averaging: investing a fixed amount at regular intervals (monthly, with each paycheck) regardless of market conditions. This approach automatically purchases more shares when prices are low and fewer when prices are high, reducing average cost over time and eliminating the psychological burden of timing decisions entirely.

Checking Your Portfolio Too Frequently

Research consistently shows that investors who check their portfolio more frequently make worse decisions. Frequent monitoring amplifies the emotional response to short-term fluctuations—the natural human tendency toward loss aversion causes disproportionate distress from declines relative to pleasure from equivalent gains. This emotional response drives selling at market lows (crystallizing losses) and missing the recovery that invariably follows.

For a retirement investor with a 20–40 year time horizon, daily portfolio checks are not just unhelpful—they are actively harmful. A quarterly review is sufficient for most retirement investors. Annual rebalancing (returning the portfolio to its target allocation by trimming over-weighted assets and buying under-weighted ones) is the only active management most long-term investors need.

Confusing Tax-Advantaged Accounts with the Investments Inside Them

One of the most persistent conceptual confusions in beginner investing is treating account types as if they were investment types. “I have a Roth IRA” is not an investment strategy—it is an account structure. The Roth IRA itself earns nothing; the investments held inside the Roth IRA earn returns. A Roth IRA containing only a money market fund will grow at near-zero rates despite its excellent tax structure. The same Roth IRA containing a total stock market index fund will compound meaningfully over decades. The account is the bucket; the investments are what fills it.

All 4 Accounts at a Glance: The Quick Reference Table

| Account | Tax Treatment | Annual Limit | Early Withdrawal | Best For |

|---|---|---|---|---|

| 401(k) / 403(b) | Traditional: pre-tax / Roth: after-tax | $23,000 (+ catch-up at 50+) | 10% penalty + taxes before 59½ | Everyone with employer access; capture the match first |

| Traditional IRA | Pre-tax (if deductible); tax-deferred growth | $7,000 (+ $1,000 at 50+) | 10% penalty + taxes before 59½ | High earners expecting lower retirement tax rate |

| Roth IRA | After-tax; tax-free growth and withdrawals | $7,000 (+ $1,000 at 50+) | Contributions anytime; earnings penalized before 59½ | Young investors; those expecting higher future tax rates |

| HSA | Triple tax advantage (in, growth, out) | ~$4,150 individual / ~$8,300 family | Penalty-free for medical; taxed (non-medical) before 65 | HDHP enrollees; the ultimate long-term healthcare fund |

| Taxable Brokerage | After-tax; capital gains on profits | No limit | No penalty; capital gains taxes apply | Mid-term goals; early retirees; excess beyond other limits |

Note: Contribution limits are updated periodically by the IRS. Verify current limits at irs.gov before making contributions each year.

4. Securing Your Empire: Tools for the Investor

Once you start building wealth, you become a target. Digital security is no longer optional; it is a requirement for asset protection.

Furthermore, ensure your physical environment supports your financial focus. Investing requires research and concentration. Upgrade your home office gadgets to create a distraction-free zone, or ensure your budget laptop is secure and dedicated to your work and finances.

Investment Account FAQs: Beginner Questions Answered

Can I have both a 401(k) and an IRA?

Yes. The 401(k) and IRA are separate accounts with separate contribution limits—maxing one does not affect your ability to contribute to the other. High earners may face deductibility limitations on Traditional IRA contributions if they also participate in a workplace retirement plan, but Roth IRA contributions (subject to income limits) and non-deductible Traditional IRA contributions are always available regardless of 401(k) participation.

What happens to my 401(k) if I leave my job?

You have four options: leave it with your former employer’s plan (acceptable if the investment options are good), roll it over to your new employer’s 401(k) plan (good if the new plan has better options), roll it over to a Traditional IRA at a brokerage of your choice (typically the best option for investment flexibility and cost), or cash it out (almost always the worst choice—triggers income taxes and a 10% early withdrawal penalty, destroying significant accumulated value). Always execute a direct rollover rather than taking a distribution to avoid mandatory withholding and rollover deadline complications.

How much should I invest each month?

The right amount is the maximum you can sustain consistently without depleting your emergency fund or taking on debt. The commonly cited target of 15% of gross income toward retirement is a useful benchmark—it includes any employer match in the calculation. For those starting later, catching up may require a higher savings rate. For those starting early, even 10% invested consistently produces excellent long-term outcomes through the power of compound growth over decades.

Is investing the same as gambling?

No—the distinction is fundamental. Gambling is a zero-sum game where money transfers from losers to winners and the house takes a guaranteed cut; the expected value of gambling is negative. Long-term investing in broad market index funds is participation in the collective productive output of thousands of companies. Over long time horizons, the economy grows, company earnings increase, and stock prices reflect that growth. The expected value of long-term diversified investing is positive. Short-term speculation in individual stocks or options behaves more like gambling; long-term, diversified, passive investing is a fundamentally different activity.

Essential Gear for the Serious Investor

Protecting your physical documents and your digital assets is just as important as choosing the right stock.

As you open these accounts, you will generate critical paperwork: beneficiary forms, account deeds, backup codes for 2FA, and perhaps even a hardware wallet seed phrase. A fireproof and waterproof document bag ensures that a physical disaster at home does not wipe out your access to your financial future. It is a small insurance policy for your peace of mind.

Check Price on Amazon

For the modern investor diversifying into digital assets (crypto), leaving funds on an exchange is risky. The saying goes, “Not your keys, not your coins.” A hardware wallet takes your assets offline, making them immune to online hacks. Even if you are just starting, understanding cold storage is a key part of advanced financial literacy, much like reading the top finance books.

Check Price on AmazonFinal Verdict: Just Start

The perfect investment account is the one you actually fund. Do not get bogged down in analysis paralysis. Start with your 401(k) match, then open a Roth IRA. These simple steps, taken early, utilize the most powerful force in the universe: compound interest.

Your future self is begging you to start today. Treat this guide as your checklist, open your first account, and begin the journey to financial independence.