5 Simple Steps to Create a Zero-Based Budget (Checklist for Financial Freedom)

Most people think a budget is a constraint—a mathematical prison that stops you from having fun. This is false. A budget is permission. It is a tool that allows you to spend money guilt-free because you have already decided where every dollar is going.

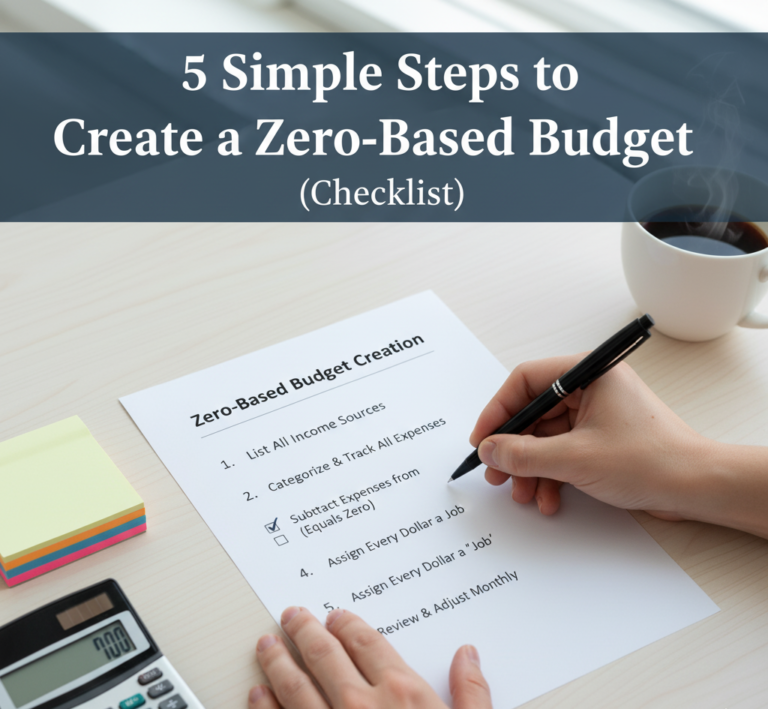

The Zero-Based Budget (ZBB) is the gold standard of personal finance. It is the method used by corporations and millionaires alike to maximize efficiency. The concept is simple: Income minus Expenses equals Zero. This doesn’t mean you have zero dollars in your bank account; it means every dollar has been assigned a “job”—whether that job is paying rent, buying groceries, or growing in your investment account.

If you have read the top 10 books on personal finance, you know that tracking is the first step to wealth. This guide takes that theory and turns it into a practical, step-by-step checklist to revolutionize your relationship with money.

Zero-Based Budgeting vs. Other Methods: Why ZBB Wins

Before building your first zero-based budget, it is worth understanding why this method consistently outperforms the alternatives that most people default to. The budgeting method you choose determines not just how you track money, but how you think about it—and that mental model has compounding effects over years and decades.

| Method | How It Works | The Problem | ZBB Advantage |

|---|---|---|---|

| Zero-Based Budget | Every dollar assigned a job. Income − Expenses = $0 | Requires monthly effort | Maximum intentionality; no money “disappears” |

| 50/30/20 Rule | 50% needs, 30% wants, 20% savings | Too rigid for variable incomes; ignores debt payoff urgency | ZBB adapts to any income level and prioritizes goals dynamically |

| Percentage-Based | Fixed % to each category | Real life doesn’t fit percentages; ignores seasonal variation | ZBB is rebuilt monthly, capturing reality not theory |

| “Just Track It” | Log spending after the fact | Reactive, not proactive; overspending already happened | ZBB assigns money before it’s spent, preventing overspend |

| No Budget | Hope for the best | Money disappears without explanation; goals never funded | ZBB reveals exactly where every dollar went and why |

The 50/30/20 rule is the most commonly recommended alternative, and while it is better than no budget, it has a fundamental design flaw: it normalizes spending 30% of income on “wants” regardless of your financial situation. A person carrying high-interest debt, aggressively saving for a home down payment, or building an emergency fund from zero needs a method that can redirect that 30% to urgent priorities. Zero-based budgeting provides exactly that flexibility because the allocation is rebuilt from scratch every month based on your current reality.

The Psychology of Budgeting: Why Most People Quit (And How Not To)

More budgets are abandoned than sustained. Understanding why helps you design yours for durability from the start rather than discovering the pitfalls through repeated failure. The behavioral economics of personal finance is well-researched, and the patterns of budget abandonment are consistent.

The most common reason people quit budgeting is a phenomenon called budget shame. When actual spending exceeds a budgeted category—and it will, especially in the first few months—people experience a strong emotional response of guilt or failure. That feeling, combined with the effort required to update the budget, makes avoidance the path of least resistance. The budget stops being checked, then stops being updated, then ceases to exist as a practical tool.

The solution is reframing what a budget overage means. An overage is not failure—it is information. It tells you that your initial estimate for that category was too low, or that an irregular expense appeared that you had not planned for. Both are fixable. The appropriate response is to adjust the category allocation next month, not to abandon the system. Treating the budget as a living document that improves through iteration rather than a perfect plan that must be executed flawlessly is the mindset shift that separates the people who sustain financial discipline from those who cycle through budget restarts every January.

Budget rigidity is the second most common failure mode. Budgets built with no flexibility—every dollar pre-allocated with no buffer—fail at the first real-world contact with an irregular expense, a price increase, or an unexpected social invitation. Building a small “miscellaneous” or “flex” category of $50–$150 per month into your zero-based budget absorbs these minor shocks without derailing the entire system.

Step 1: Calculate Your True Monthly Income

You cannot manage what you do not measure. The first step is to determine exactly how much money flows into your life every month. This isn’t just your salary; it’s everything.

The Income Audit

Sit down and list every source of income. Be realistic—use your net pay (what actually hits your bank), not your gross pay.

- Primary Job: Your regular paycheck.

- Side Hustles: Do you freelance using your home office setup? Include that average income.

- Digital Sales: Did you recently sell an old device after upgrading to one of the top budget laptops? Include that cash influx.

- Passive Income: Dividends or interest from your savings.

Handling Variable and Irregular Income

The income audit is straightforward for salaried employees. For freelancers, contractors, gig workers, and small business owners, variable income creates a planning challenge that requires a specific strategy. Budgeting from a number that fluctuates month to month can feel impossible—but it is not.

The most reliable method for variable income budgeting is the baseline approach: identify the lowest monthly income you have received over the past 12 months and build your budget around that number as your guaranteed baseline. Any income above that baseline in a given month is allocated in a predetermined priority order—first to emergency fund, then to debt, then to savings goals—rather than flowing into discretionary spending by default.

For those with genuinely unpredictable income swings, a holding account strategy works well: all income is deposited into a separate holding account rather than directly into your spending account. On the first of each month, you transfer a fixed “salary” to yourself—equal to your baseline income—into your budgeted spending account. This creates artificial income smoothing that makes zero-based budgeting possible even in highly volatile income environments.

The Gross vs. Net Income Trap

Using gross income to budget is one of the most common first-time budgeting mistakes and one of the most consequential. Gross income—your salary before taxes, health insurance premiums, retirement contributions, and other pre-tax deductions—can be 20–35% higher than the net income that actually reaches your bank account. Building a budget around gross income produces a plan that is perpetually $500–$1,500 per month more generous than your actual spending capacity, guaranteeing budget failure from day one.

Always start with net take-home pay. If your employer withholds health insurance premiums, retirement contributions, or HSA contributions from your paycheck before it arrives, those are already allocated—treat them as existing budget categories rather than income to be allocated.

Step 2: List Every Single Expense (The “No-Hiding” Rule)

This is where most people fail. They list rent and car payments but forget the “invisible” expenses like daily coffee or digital subscriptions. To build a zero-based budget, you must be ruthless.

The “Four Walls” & Beyond

Start with the essentials (Shelter, Utilities, Food, Transportation) and then move to the discretionary.

1. Food Costs (The Budget Killer)

Food is often the biggest variable expense. You can drastically lower this by planning. Instead of ordering takeout, budget for groceries to make quick and healthy weeknight dinners. Using efficient tools like the top 5 kitchen gadgets worth the money can make home cooking feel less like a chore and more like a strategy.

2. The Digital Leak

Check your bank statement for recurring subscriptions. Do you really need five streaming services? Use one of the 5 free password managers to audit your accounts and cancel what you don’t use.

3. The Irregular Expense Problem: The Category Most Budgets Miss

The most structurally overlooked expense category in most budgets is not discretionary spending—it is irregular, predictable expenses that simply do not occur monthly. Car registration, annual insurance premiums, quarterly tax payments, holiday gifts, back-to-school shopping, vehicle maintenance, and home repairs all fall into this category. They are predictable in the sense that they will occur; they just do not fit neatly into a monthly recurring schedule.

The standard budgeting response—to treat these as “surprise” expenses when they arrive and cover them by raiding other categories or using a credit card—is one of the most reliable ways to blow a budget repeatedly without ever understanding why. The solution is a sinking fund system: dividing each annual or semi-annual expense by 12 and budgeting that monthly amount into a dedicated savings category. When the bill arrives, the money is already waiting.

A car registration that costs $240 annually becomes a $20 monthly sinking fund contribution. A $600 holiday gift budget becomes $50 per month saved from January through December. An estimated $1,200 annual vehicle maintenance budget becomes $100 per month. Added together, these sinking fund contributions may total $200–$400 per month—real money that, unplanned for, becomes a budget crisis each time one of these expenses arrives.

4. The Subscription Audit: Finding Your Hidden Monthly Burn

The average American household pays for more than a dozen recurring subscription services and is aware of fewer than half of them. Streaming services, software subscriptions, app store auto-renewals, gym memberships, magazine subscriptions, cloud storage upgrades, and premium tiers of free services collectively represent a “subscription tax” that quietly compounds month after month.

A proper subscription audit requires pulling 90 days of bank and credit card statements and highlighting every recurring charge. List each subscription, its monthly cost, and when you last actively used it. Apply a simple test: if this service disappeared tomorrow, would you notice within a week? If not, cancel it. Most people who complete this exercise find $50–$150 per month in subscriptions they had genuinely forgotten about—money that, redirected to a savings goal, compounds meaningfully over a year.

Step 3: Categorize and Prioritize (Needs vs. Wants)

Now that you have a list, organize it. This aligns with the 7 habits of people who are good with money: they value value over price.

The Goal-Setting Layer

Your budget should reflect your dreams. If you don’t prioritize your goals, they will never happen.

- Travel Fund: Are you dreaming of visiting the cheapest European cities? Create a specific category for this. Use the checklist for how to plan a trip to estimate exactly how much you need to save monthly.

- Debt Destruction: If you have debt, create a category for “Extra Debt Payments.” Paying this down is the fastest way to improve your credit score.

- Self-Care: Budget for your well-being. Whether it’s the products for your essential skincare routine or a gym membership, categorize it so you can do it guilt-free, following the ultimate self-care checklist.

The Recommended Budget Category Framework

Most people try to track too many categories in their first budget, creating complexity that makes the system feel overwhelming. The following framework uses broad-enough categories to be manageable while specific enough to reveal meaningful patterns in your spending.

Rent/mortgage, utilities, insurance, repairs

Car payment, gas, insurance, maintenance, transit

Groceries + dining out (tracked separately)

Emergency fund, retirement, specific goals

Minimum payments + accelerated payoff amount

Clothing, self-care, hobbies, entertainment

Prioritizing Competing Goals: The Financial Hierarchy

One of the most common budgeting decision points is determining which financial goal to fund when money is limited. Should you pay off debt aggressively or save for an emergency fund? Should you maximize retirement contributions or save for a home down payment? Having a clear priority hierarchy eliminates the paralysis of competing goals and ensures every surplus dollar is directed where it produces the most value.

A widely recommended priority order for most financial situations works as follows. First, build a small starter emergency fund of $1,000—enough to handle minor emergencies without reaching for a credit card. Second, capture any employer 401(k) match in full—this is a 50–100% guaranteed return on investment that no other financial move can compete with. Third, eliminate high-interest debt (typically anything above 6–7% interest rate) using either the avalanche method (highest interest rate first, mathematically optimal) or the snowball method (smallest balance first, psychologically motivating). Fourth, build a full three-to-six month emergency fund. Fifth, invest for long-term goals through tax-advantaged accounts. Only after this sequence is addressed should significant money flow to discretionary savings goals like travel funds or luxury purchases.

Step 4: The Zero Calculation (Giving Every Dollar a Job)

This is the core of the ZBB method. You must subtract your expenses from your income until the result is exactly zero.

What if you have money left over?

If you do the math and have $200 left over, you aren’t done. You don’t leave that money “floating” in your checking account—it will disappear. You must assign it a job.

Assigning the Surplus:

- Invest It: Move it to one of the 4 types of investment accounts (like a Roth IRA).

- Emergency Fund: Build your safety net.

- Experience Fund: Save for gear like the ultimate packing list for Europe or essential carry-on items.

What if you are negative?

If your expenses exceed your income, you have a crisis. You must cut costs immediately. Look at your discretionary spending. Are you spending too much on impulse buys via your phone? Use our guide on reducing screen time to stop the scroll-and-shop cycle.

Closing a Deficit: A Prioritized Expense Reduction Framework

A negative calculation—where expenses exceed income—is confronting but common, especially when building a budget for the first time and seeing the full picture clearly for the first time. The path to balance requires reducing expenses, increasing income, or both. The order in which you approach expense cuts matters: protecting essential spending while targeting discretionary spending first produces better life outcomes than indiscriminate cuts.

Tier 1 cuts are painless: cancelled forgotten subscriptions, eliminated impulse purchases, reduced takeout frequency in favor of planned home cooking, renegotiated recurring bills (insurance premiums, internet plans, phone plans—a single call to your provider often yields $20–$50 per month in savings). These cuts produce real savings with minimal lifestyle impact and should be exhausted before touching anything else.

Tier 2 cuts require deliberate trade-offs: reducing entertainment budgets, scaling back clothing and personal care spending, temporarily pausing discretionary savings goals to stabilize the budget, carpooling or using transit instead of driving. These cuts affect quality of life noticeably but temporarily—they are the tools of a financial sprint, not a permanent lifestyle.

Tier 3 cuts involve structural life changes: moving to lower-cost housing, selling a vehicle and using alternatives, taking on a roommate, or significantly downscaling lifestyle expenses. These are significant decisions with long adjustment periods and should only be considered when Tier 1 and 2 cuts have been exhausted and the deficit remains material.

Increasing Income: The Other Half of the Equation

Most budgeting advice focuses exclusively on expense reduction, which is directionally correct but incomplete. Expense reduction has a mathematical floor—you cannot cut below zero—while income has no ceiling. For people whose expenses are already lean and whose deficit cannot be closed through cuts alone, income augmentation is the only viable path.

The fastest income augmentation strategies: overtime or additional hours at your current employer (the lowest-friction path since the relationship and tax documentation already exist), freelancing skills you already possess in your primary field (writing, design, coding, consulting, tutoring), selling items you own but do not need (a systematic home purge of unused electronics, clothing, furniture, and sporting goods can generate $500–$2,000 in a single weekend), and renting assets you already own (a spare room, a parking space, a vehicle during unused hours through peer-to-peer platforms).

A $300 monthly income increase has the same budget impact as $300 in expense cuts but with none of the lifestyle sacrifice. Pursuing both sides of the equation simultaneously—even modest improvements on each—compounds quickly.

Step 5: Track and Adjust (The Execution Phase)

A budget on paper is useless if you don’t follow it. You must track your spending throughout the month to ensure you stay within your limits.

The Daily/Weekly Check-in

Consistency is key. This aligns with the top 5 habits of highly effective people: they are disciplined.

- Use Apps: Leverage the best productivity apps to log expenses on the go.

- Time Block It: Don’t rely on willpower. Use time blocking to schedule a 15-minute budget review every Friday.

- Morning Review: Incorporate a quick bank balance check into your morning routine. Awareness prevents overspending.

If you find yourself avoiding this step, you are dealing with fear, not math. Use the strategies in 7 ways to beat procrastination to force yourself to face the numbers.

The Tracking System: Manual vs. Automated

The best tracking system is the one you will actually use consistently. This sounds obvious, but it is the principle most people violate by adopting a highly sophisticated system they abandon after two weeks rather than a simple one they maintain for two years. The goal is sustainability over optimization.

Manual tracking—entering every transaction by hand into a spreadsheet or physical planner—has a powerful psychological benefit: the friction of recording each purchase creates a natural pause that reduces impulse spending. Research in behavioral economics consistently shows that the act of manually logging a purchase creates a mild aversion response that reduces the frequency of future similar purchases. The disadvantage is time: manual tracking takes 5–10 minutes per day, which compounds into real time commitment over months.

Automated tracking via apps like YNAB (You Need A Budget), Mint, Personal Capital, or Copilot connects to your bank accounts and categorizes transactions automatically. Setup takes 30–60 minutes; ongoing maintenance takes 5–10 minutes per week to review and correct miscategorized transactions. The significant advantage is completeness—automated systems catch every transaction, including the small ones that manual trackers consistently forget to log. The disadvantage is that the reduced friction of automatic categorization also reduces the psychological engagement that makes manual tracking behaviorally effective.

A hybrid approach—automated transaction import combined with a weekly manual review and category confirmation—captures the completeness benefits of automation while preserving the conscious engagement that drives behavioral change.

The Monthly Budget Reset: Why ZBB Requires a Monthly Ritual

The defining characteristic of zero-based budgeting that distinguishes it from every other method is the monthly reset. Unlike a static budget that carries the same allocations forward indefinitely, ZBB requires rebuilding the budget from zero at the start of each month. Every dollar of income is reassigned; every expense category is reconsidered. Nothing is automatically rolled over.

This monthly ritual serves three functions. It forces conscious awareness of your financial situation at least once per month—eliminating the “I’ll check the budget later” avoidance that allows small problems to compound into crises. It allows real-time adaptation to changing circumstances: a month with an unusually high utility bill, a car repair, or a bonus income payment is reflected in that month’s budget without waiting for a quarterly review. And it keeps financial goals visible and current—a travel fund that is three months from its target is a different budget priority than one that is 18 months away.

Schedule your monthly budget reset as a recurring calendar appointment, ideally a few days before the month begins. Thirty minutes of deliberate budget building at the start of each month has a documented return-on-time that exceeds almost any other financial activity.

Zero-Based Budgeting for Couples and Families

Money is consistently cited as one of the primary sources of conflict in long-term relationships. The zero-based budget, when approached as a shared exercise rather than one partner’s project, can transform financial conversations from flashpoints into structured, productive planning sessions. But doing this well requires specific adaptations to the individual framework.

The Joint Budget Meeting

The most common failure mode in couples budgeting is one partner doing all the work and presenting the other with a completed budget to approve. This dynamic, however well-intentioned, creates a power imbalance and leaves the uninvolved partner with no emotional investment in following the plan. Both partners must build the budget together for it to function as a shared commitment rather than a household policy handed down from on high.

A monthly budget meeting of 30–60 minutes, with both partners present and actively contributing, is the structural foundation. The agenda: review last month’s actual spending against the budget (no judgment, only analysis), discuss any upcoming irregular expenses or changed circumstances, and build next month’s allocations together. Treating this meeting as a protected calendar appointment—equal in priority to any other commitment—signals to both partners that financial management is a shared household responsibility.

Fun Money: The Budget’s Pressure Valve

One of the most effective features of a couples’ zero-based budget is the “personal spending” or “fun money” allocation: a fixed monthly amount that each partner spends however they choose, without explanation or joint approval required. This amount—which might range from $50 to $300 depending on income—serves as the budget’s pressure valve. It eliminates the resentment of feeling that every personal purchase requires justification, which is the single most reliably corrosive experience in shared budgeting.

Partners who have full autonomy over a designated personal amount are significantly more supportive of discipline in shared budget categories. The feeling of financial agency—even over a small amount—reduces the psychological cost of budgeting as a whole.

Using Zero-Based Budgeting to Destroy Debt Faster

The zero-based budget is arguably the most powerful debt payoff tool available because it makes the debt payoff decision explicit every single month rather than leaving it to the automatic minimum payment. The difference in outcome between minimum payments and accelerated payoff on consumer debt is dramatic: a $5,000 credit card balance at 22% interest paid at the minimum payment rate takes approximately 17 years to eliminate and costs $7,000+ in interest. The same balance paid with an extra $150 per month is eliminated in 28 months and costs $1,300 in interest—a $5,700 difference from a single budget line change.

The Debt Avalanche vs. Debt Snowball: Choosing Your Method

Once your budget has identified the amount available for extra debt payoff each month, you need a strategy for which debt to target first. Two methods dominate the personal finance community, and both work—the right one depends on whether you are motivated more by mathematics or psychology.

The debt avalanche method directs extra payment to the highest interest rate balance first, regardless of balance size. This is mathematically optimal—you pay the least total interest and eliminate debt in the shortest total time. It is the correct choice for people who are sufficiently motivated by the long-term financial outcome and can sustain effort over the months or years it may take to eliminate a large high-interest balance before seeing a debt disappear entirely.

The debt snowball method targets the smallest balance first, regardless of interest rate. Mathematically suboptimal, it produces faster visible victories—the psychological “win” of eliminating an account entirely. Research by behavioral economists has shown that these quick wins increase the probability of sustained debt payoff effort, often producing better real-world outcomes than the mathematically superior avalanche method that people abandon before it works.

A practical hybrid: if your smallest balance and highest interest rate balance are within 10–15% of each other in payoff timeline, choose the higher interest rate target. If they differ substantially, consider the snowball for the motivational benefits.

Building Your Emergency Fund Inside a Zero-Based Budget

The emergency fund is the financial foundation that makes all other budget goals possible. Without it, every unexpected expense—a car repair, a medical bill, a home appliance failure—becomes a crisis that forces debt, disrupts savings goals, and creates a cycle of perpetual financial instability. With it, these events become planned inconveniences absorbed by a dedicated pool of money set aside for exactly this purpose.

In a zero-based budget, the emergency fund is a line item like any other—not a leftover after other goals are funded, but a deliberate, prioritized allocation. The starter emergency fund target of $1,000 is achievable in 2–4 months for most households with focused effort: a temporary spending reduction, a small income augmentation, and consistent contribution. The full 3–6 month emergency fund is a longer-term goal that is funded incrementally over 12–24 months while other financial goals run in parallel.

The emergency fund should be held in a separate, high-yield savings account—physically separate from your checking account to reduce the temptation to raid it for non-emergencies, but accessible within 1–2 business days for genuine emergencies. High-yield savings accounts currently offer meaningfully higher interest rates than traditional savings accounts, allowing your emergency fund to grow passively while it waits.

The Zero-Based Budget Toolkit

While you can budget on a napkin, having the right tools makes the process enjoyable and sustainable. These products help bridge the gap between planning and execution.

For those who prefer pen and paper to spreadsheets, this is the ultimate tool. It forces you to write down your goals, track your daily spending, and perform a monthly review. The physical act of writing reinforces the neural pathways associated with discipline. It includes pockets for bills and stickers to make the process visual and engaging.

Check Price on Amazon

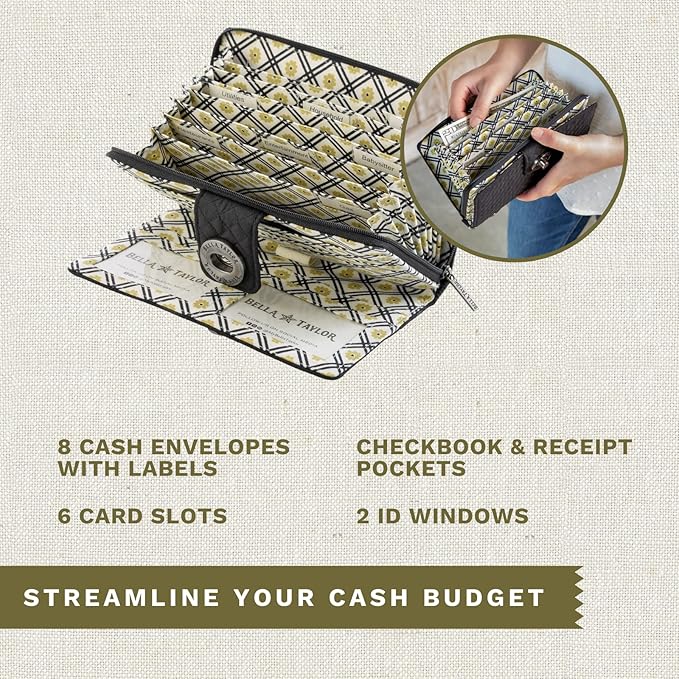

If you struggle with overspending on categories like groceries or entertainment, the “Cash Envelope System” is the cure. You withdraw the exact amount of cash budgeted for that category and put it in the envelope. When the cash is gone, you stop spending. This wallet organizes your envelopes stylishly, replacing your standard wallet with a budgeting system you carry everywhere.

Check Price on AmazonZero-Based Budget FAQs: The Most Common Questions Answered

Do I need to budget to the dollar?

Yes and no. The zero-based budget requires that every dollar is assigned a category—that is the defining feature of the method. But “assigned” does not mean “spent on a single predictable item.” A $100 “flex” or “miscellaneous” category is a legitimate budget line. What ZBB prohibits is leaving money unassigned, floating in your account without a declared purpose. An unassigned $200 is universally spent on nothing memorable and retained as nothing useful.

What do I do when a large unexpected expense blows my budget?

This is where the budget’s adaptability matters. A true emergency expense—one your emergency fund exists to cover—should be drawn from that fund, which is then replenished in the following month’s budget. For unexpected expenses that are not true emergencies (a concert you did not plan for, a sale on something you wanted), the ZBB process requires moving money from another category to fund it. This trade-off is deliberate and visible: to spend $100 unplanned on entertainment, you must consciously reduce another category by $100. This friction is the point—it makes every unplanned expense a conscious choice.

Is zero-based budgeting too time-consuming?

The initial setup—auditing income, listing all expenses, and building the first budget—takes two to three hours. Each subsequent monthly reset takes 20–45 minutes once you have an established template. Weekly check-ins take 5–10 minutes. In total, an effective zero-based budget system requires approximately one to two hours per month of active engagement. The return on that investment—documented financial progress, reduced financial anxiety, funded savings goals—makes it one of the highest-return-per-hour activities available in personal finance.

Should I budget monthly or by paycheck?

Monthly budgeting works well for salaried employees paid once or twice per month. For weekly or biweekly pay schedules, some people find it more natural to budget by paycheck—assigning each paycheck to specific expenses and savings goals as it arrives—rather than building a monthly plan. Both approaches work; the key is consistency. If monthly planning feels overwhelming, start by budgeting each paycheck individually until the habit is established, then transition to the monthly framework as your financial fluency grows.

The Complete Zero-Based Budget Checklist

Use this master checklist at the start of every month to build your budget from scratch. Complete every item before the month begins.

📋 Step 1: Income

- Calculate net monthly income from all sources

- Note any variable income using the 3-month minimum baseline

- Include side hustle or passive income averages

📋 Step 2: Expenses

- List all fixed monthly expenses (rent, loan payments, insurance)

- List all variable expenses with realistic estimates

- Run the subscription audit — cancel anything unused

- Divide all annual/semi-annual expenses by 12 for sinking fund contributions

- Add sinking fund contributions as monthly budget line items

📋 Step 3: Categorize

- Separate all expenses into needs vs. wants

- Create dedicated goal categories (travel fund, emergency fund, etc.)

- Apply the financial priority hierarchy to goal funding order

📋 Step 4: Zero the Budget

- Subtract all expenses from income

- Assign any surplus to the highest-priority goal category

- If negative: execute Tier 1 expense cuts first, then Tier 2

- Confirm final result equals $0 before the month begins

📋 Step 5: Track and Review

- Schedule weekly 10-minute budget check-in (Friday recommended)

- Log every expense — app or manual, pick one and stick to it

- Conduct end-of-month review: actual vs. budgeted in every category

- Note category adjustments needed for next month’s build

Final Verdict: Freedom Through Discipline

A Zero-Based Budget gives you a raise without asking your boss. By finding the “leaks” in your finances—whether it’s unused subscriptions, food waste, or impulse buys—and redirecting that money toward your goals, you take control of your life.

Remember, the goal isn’t to restrict your life; it’s to fund your dreams. Whether that dream is maximizing your travel rewards for a free vacation or building a custom PC setup, the budget is the roadmap to get you there. Start Step 1 today.